【S01E10】pandas之时间序列

I. 时间序列基础

II. 生成DatetimeIndex

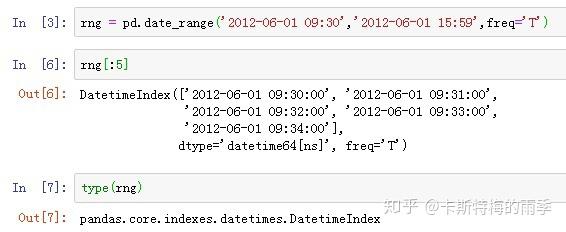

i) date_range函数

pd.date_range('2018/12/1',periods=31)

ii) 读取csv/excel时指定index_col、parse_dates关键字

df = pd.read_csv(path, engine='python', encoding='utf_8_sig',

index_col=0, parse_dates=True)

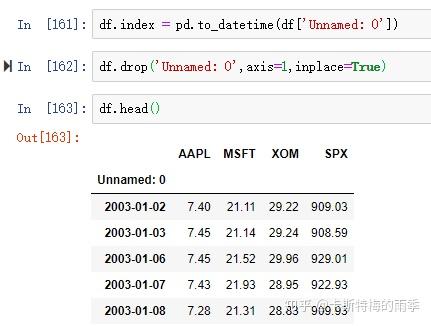

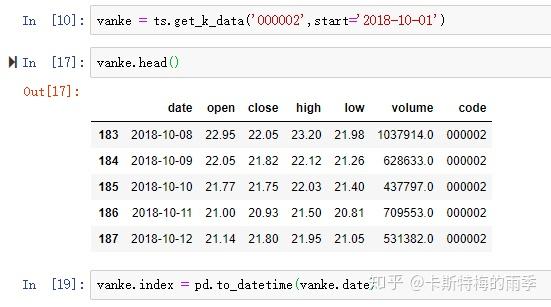

iii)df.index = pd.to_datetime(df['col'])

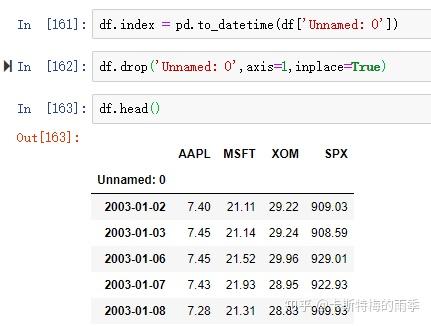

df.index = pd.to_datetime(df['Unnamed: 0'])

iv)pd.DatetimeIndex

pd.DatetimeIndex(['2018/4/14','2019/4/14'])

III. 索引为DatetimeIndex的pandas对象的索引和切片

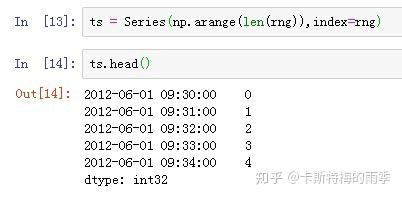

索引为DatetimeIndex的Series的索引和切片

i) 索引

ii)切片

索引为DatetimeIndex的DataFrame的索引和切片

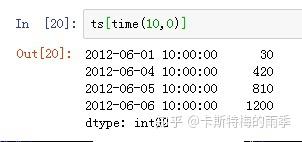

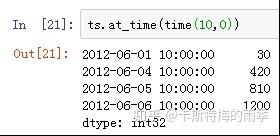

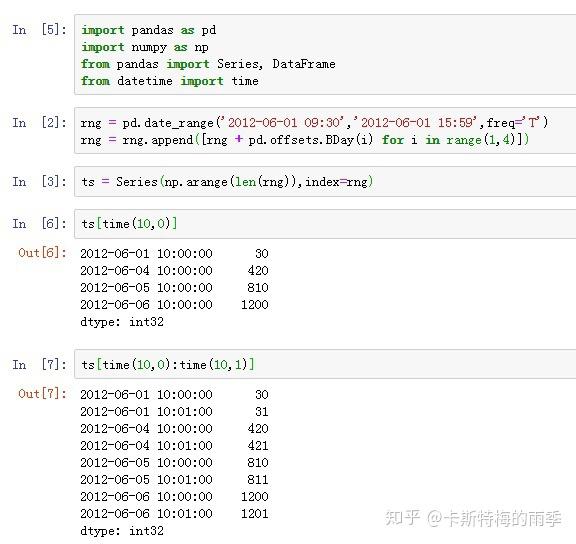

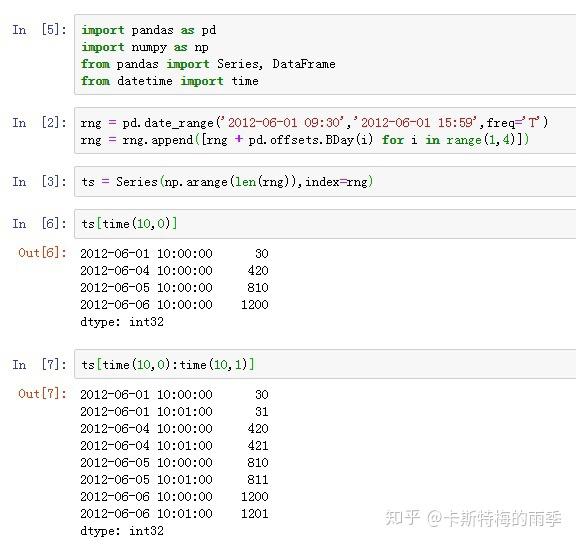

i) 索引 ps. 获取每天特定时间的数据: s[time(10,0)]

ii)切片 ps. 获取每天特定时间段的数据: s[time(10,0):time(10,1)]

VII. 将DatetimeIndex转换为PeriodIndex及其反向过程

i) 将DatetimeIndex转换为PeriodIndex————to_period

ii)将PeriodIndex转换为DatetimeIndex————to_timestamp

VIII. 重采样(resampling)

DatetimeIndex Resamping

i) 降采样

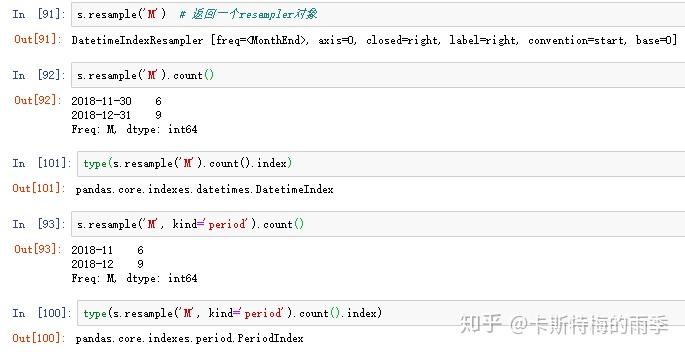

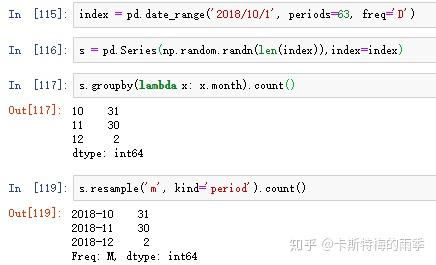

s.resample('m').count()

s.resample('m',kind='period').count()

s.resample('3min').ohlc()

ii)升采样和插值

df.resample('d').ffill(limit=2)

PeriodIndex Resamping

i) 降采样

frame.resample('a-dec').count()

ii)升采样和插值

annual_frame.resample('m', convention='end').count()

IX. 移动窗口函数(moving window function)

i) window为整数

ii)window为日期偏移量

X. 频率和时间、日期的偏移

i) 显式创建pd.tseries.offsets对象

from pandas.tseries.offsets import Hour, Minute

ii) 使用字符串别名

pd.date_range('2018/12/25', '2018/12/26',freq='4h30min' )

iii)时间、日期的偏移

s = '2018-12-08 00:08'

d = parse(s) + Minute(2)

df.loc[d]

XI. 移动数据————shift、rollforward、rollback

i) 索引保持不动,将数据前移或后移————shift

df.tip_pct = df.tip_pct.shift(1)

ii) 数据保持不动,将时间戳前移或后移————shift

s.shift(2, freq='M')

iii)通过锚点偏移量对日期进行位移

datetime(2018,3,5) + MonthEnd(2)

MonthEnd().rollforward(datetime(2018,3,5))

df.groupby(MonthEnd().rollforward).count()

时间序列(time series)指的是分布在不同时间戳(timestamp)/时期(period)上的值形成的数据集。它可以是按特定频率均匀分隔的,也可以是非均匀分隔的。

I. 时间序列基础

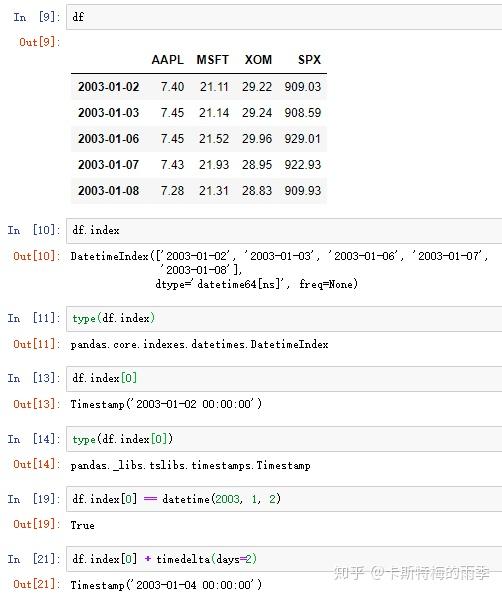

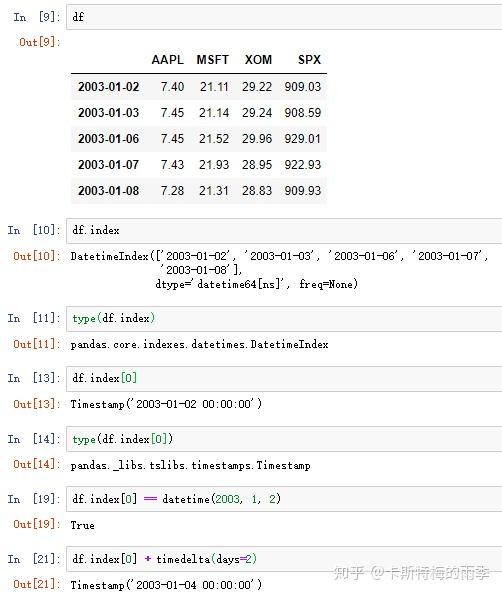

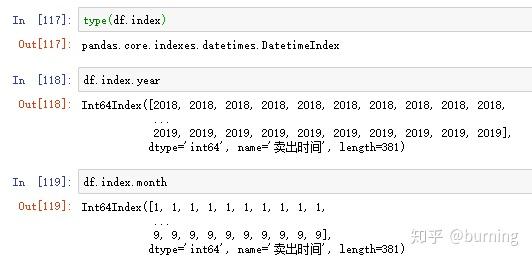

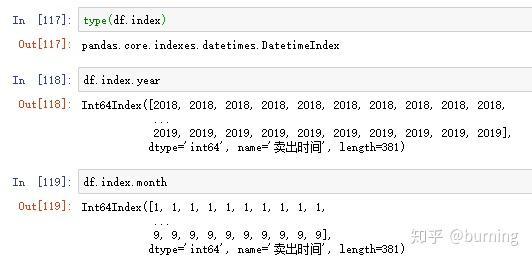

pandas中时间序列的索引分两种,即DatetimeIndex和PeriodIndex,其中最常见的是第一种。

DatetimeIndex

DatetimeIndex是由一个个Timestamp(时间戳)组成的,而Timestamp对象可以根据需要自动转化为datetime对象,所以我们可以把DatetimeIndex看作一个每个索引值都是datetime对象的索引

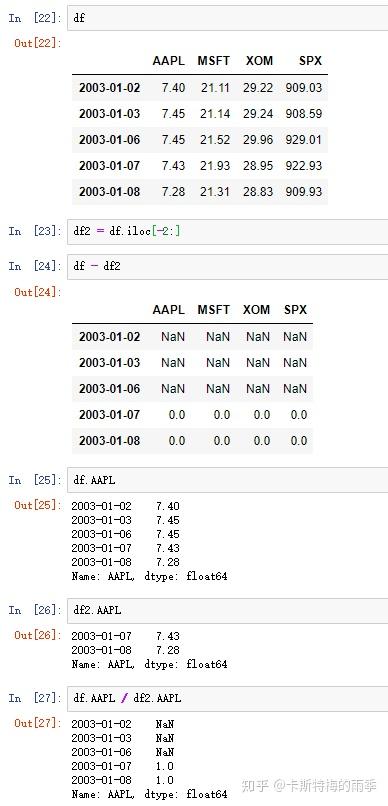

和普通的index一样,不同DatetimeIndex的Pandas对象的算术运算会自动按索引对齐

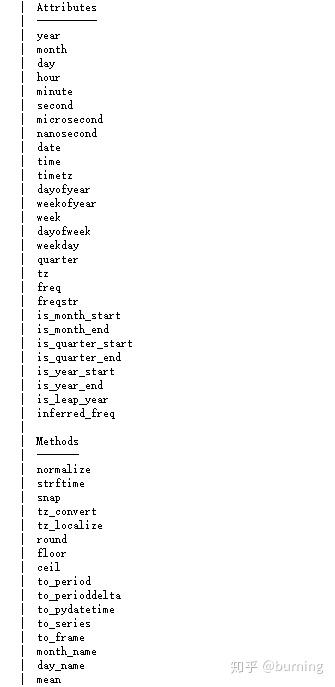

和普通索引不一样的是,DatetimeIndex还有一些独有的方法和属性

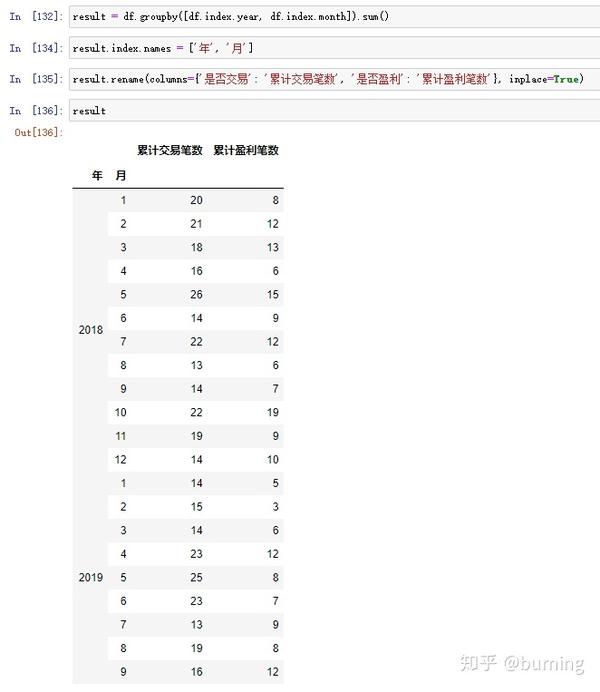

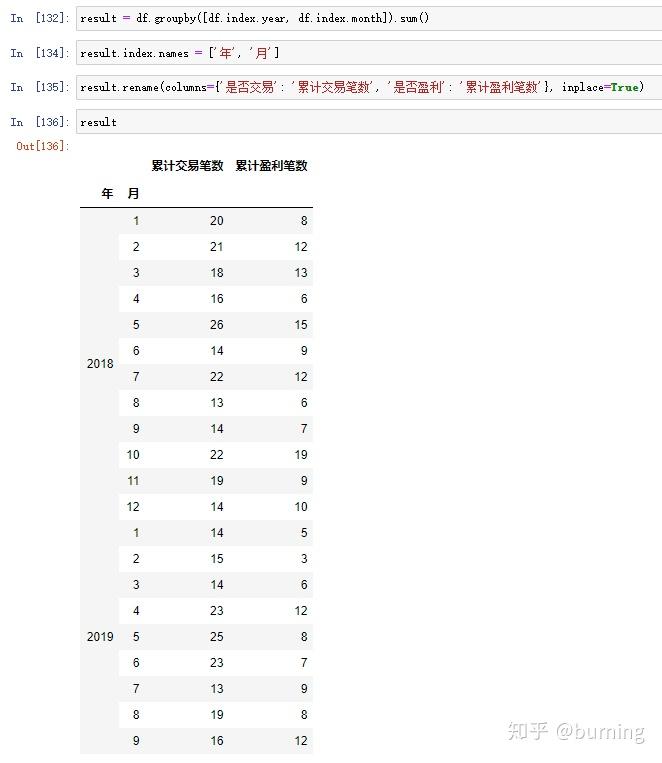

这些方法和属性有时候很有用,举个例子,假设我打算求下面这个DataFrame按年、月分组求和的累计交易笔数和累计盈利笔数就可以利用DatetimeIndex的year和month属性

再修改下列名和索引名就可以用了

PeriodIndex

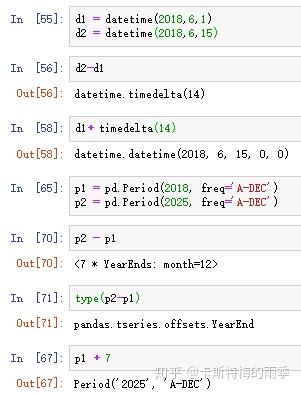

Period对象表示的是一个时间间隔,如年、月、日、时、分,PeriodIndex可以看作是每个索引值都是Period对象的索引

我们可以通过pd.Period()方法主动构造得到Period对象,此时我们需要指定频率(详细的频率及说明见下方的【时间序列基础频率表】)

Period对象还有一些跟Datetime对象类似的特性,对一个Period对象加减一个整数就相当于对其按当前频率进行位移

时间序列基础频率表

别名 偏移量类型 说明

D Day 每日历日

B BusinessDay 每工作日

H Hour 每小时

T或min Minute 每分钟

S Second 每秒钟

M MonthEnd 每月最后一个日历日

BM BusinessMonthEnd 每月最后一个工作日

Q-JAN、Q-FEB QuarterEnd 对于以指定月份结束的年度,每季度最后一月的

最后一个日历日

A-JAN、A-FEB YearEnd 每年指定月份的最后一个日历日II. 生成DatetimeIndex

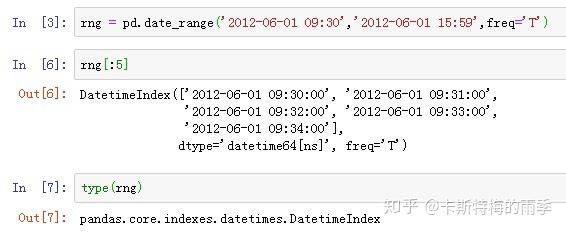

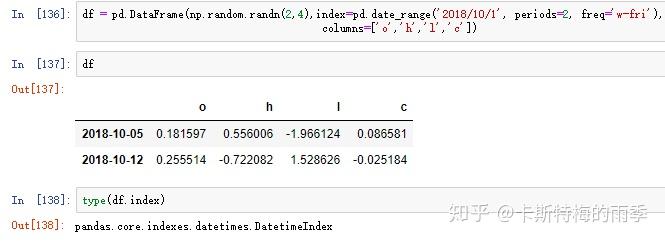

i)pd.date_range()

Return a fixed frequency DatetimeIndex

date_range(start=None, end=None, periods=None, freq=None, tz=None, normalize=False,

name=None, closed=None, **kwargs)

start : str or datetime-like, optional

Left bound for generating dates.

end : str or datetime-like, optional

Right bound for generating dates.

periods : integer, optional

Number of periods to generate.

freq : str or DateOffset, default 'D' (calendar daily)

Frequency strings can have multiples, e.g. '5H'. See

:ref:`here <timeseries.offset_aliases>` for a list of

frequency aliases.

normalize : bool, default False

Normalize start/end dates to midnight before generating date range.

name : str, default None

Name of the resulting DatetimeIndex.

closed : {None, 'left', 'right'}, optional

Make the interval closed with respect to the given frequency to

the 'left', 'right', or both sides (None, the default).

重点参数:

start

periods

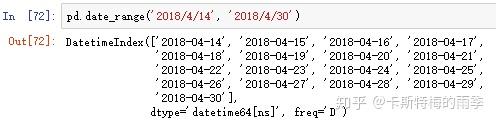

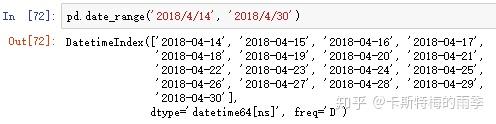

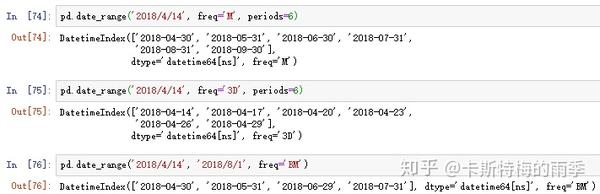

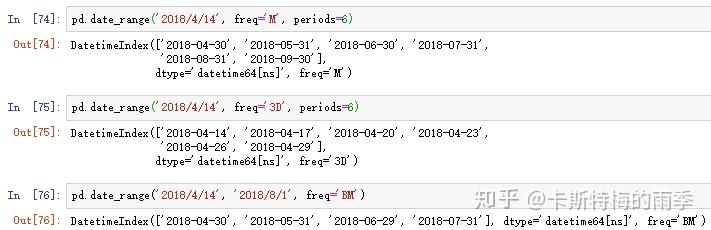

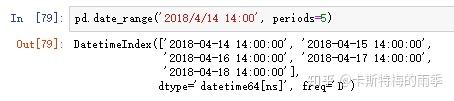

freqpd.date_range()方法可用于生成指定长度和频率的DatetimeIndex:

默认频率是'D',也可以传入其他频率;起止时间也可以只传其中一个,但此时需要指定periods,表示长度

如果timestamp包括具体的时间,date_range()方法默认会保留该时间值:

也可以选择传入 normalize=True 把时间部分去掉:

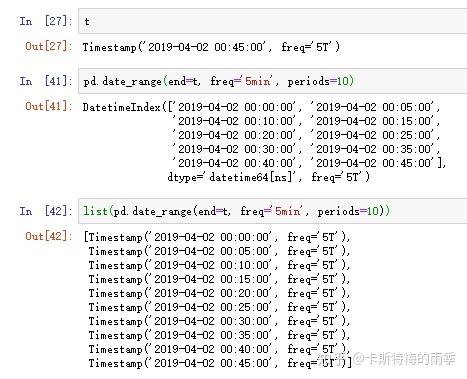

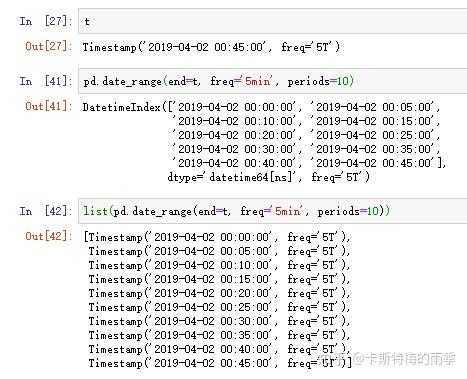

也可以调用list()方法, 将datetimeindex转化为列表:

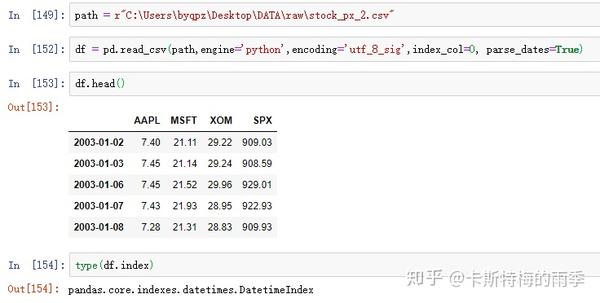

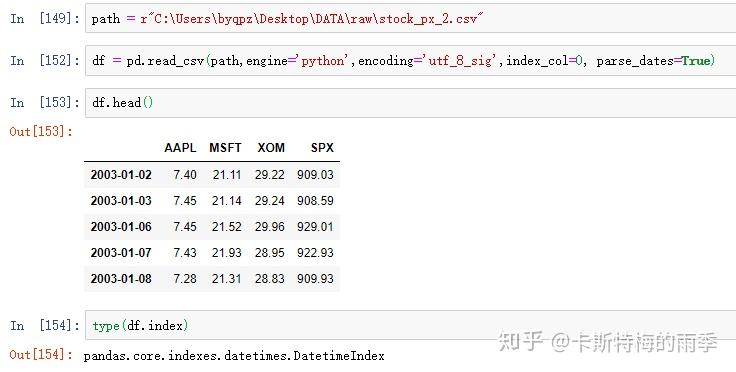

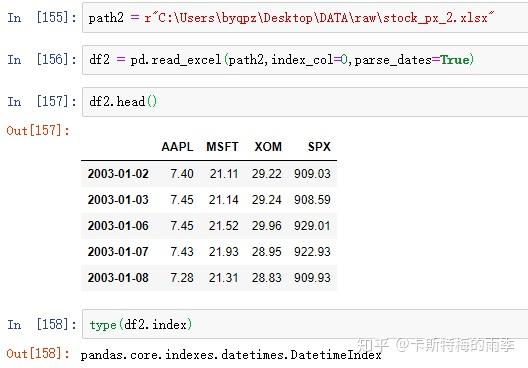

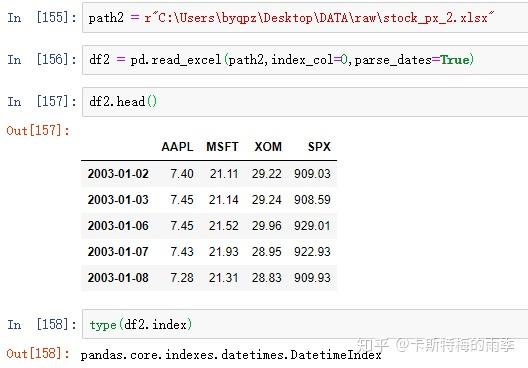

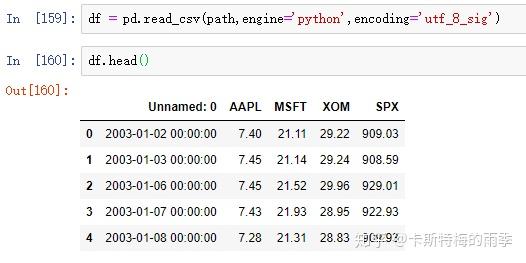

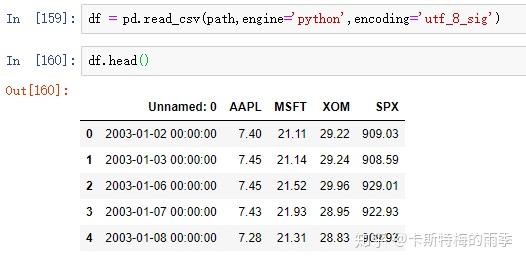

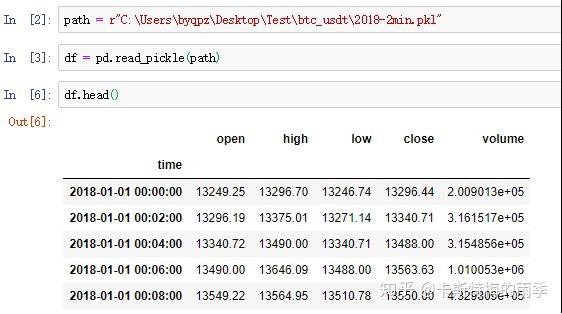

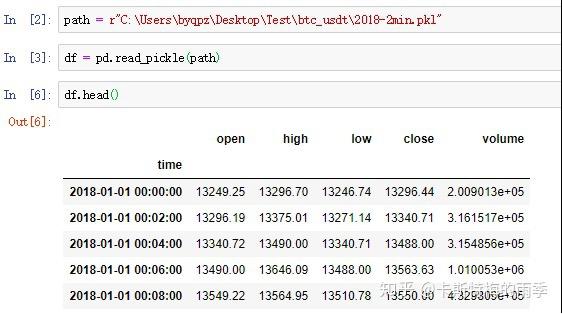

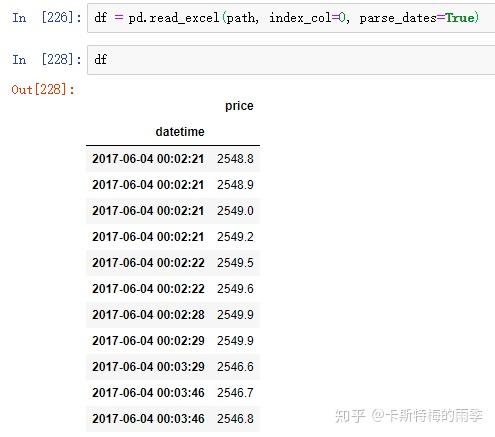

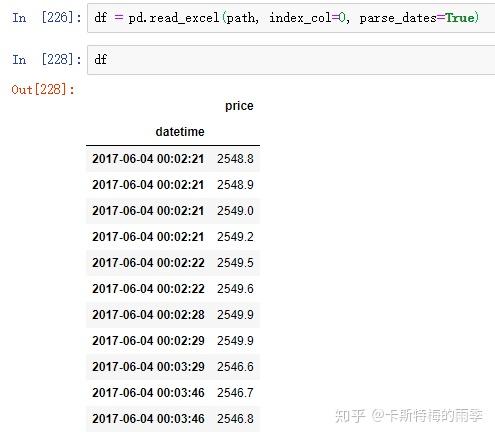

ii)pd.read_csv(path, index_col=n, parse_dates=True)/

pd.read_excel(path, index_col=n, parse_dates=True)

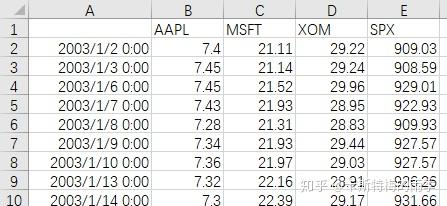

数据如下:

read_csv

read_excel

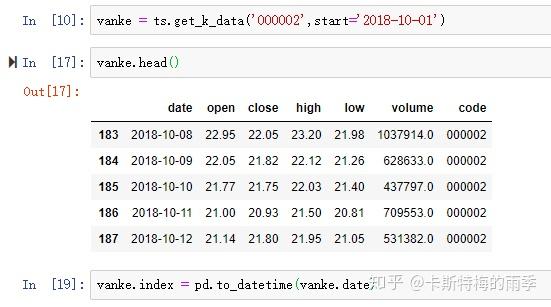

iii)df.index = pd.to_datetime(df['col'])

iv)pd.DatetimeIndex

III. 索引为DatetimeIndex的pandas对象的索引和切片

索引为DatetimeIndex的Series的索引和切片

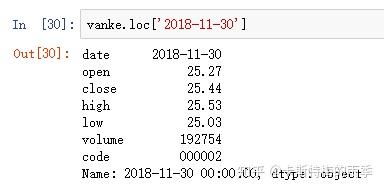

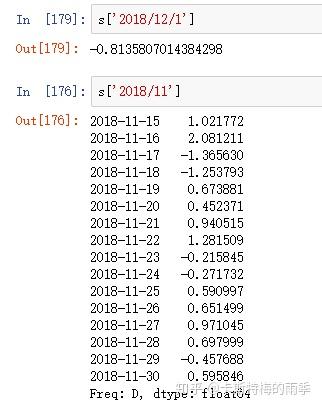

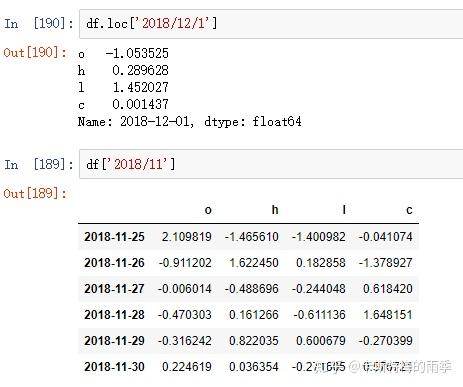

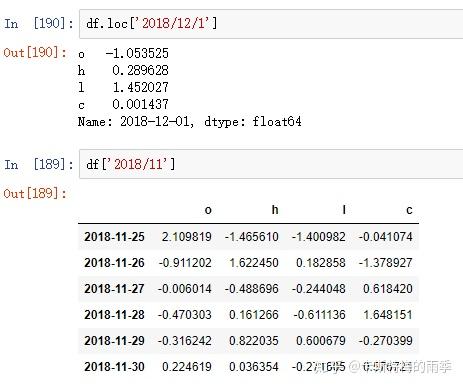

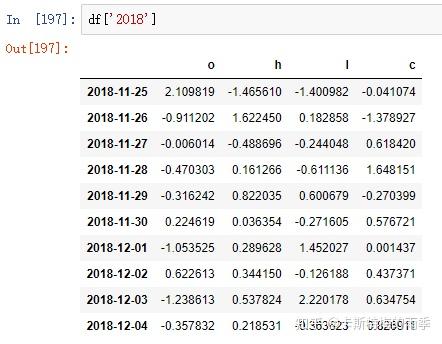

i)索引

传入一个可以被解释为时期的字符串

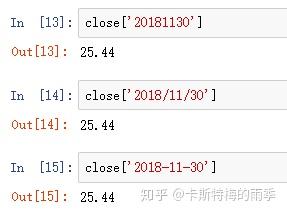

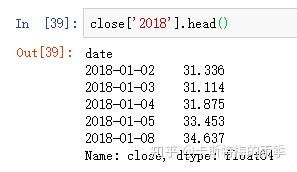

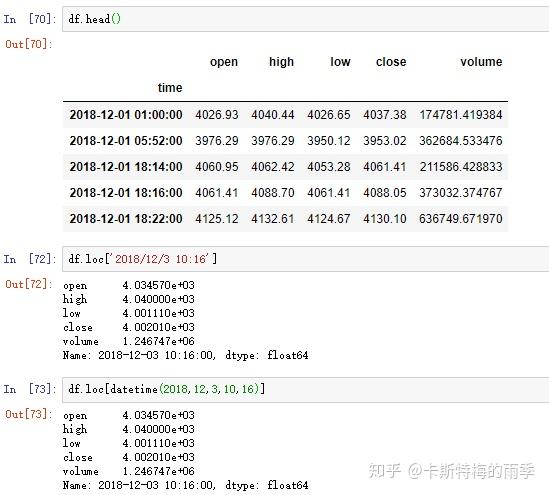

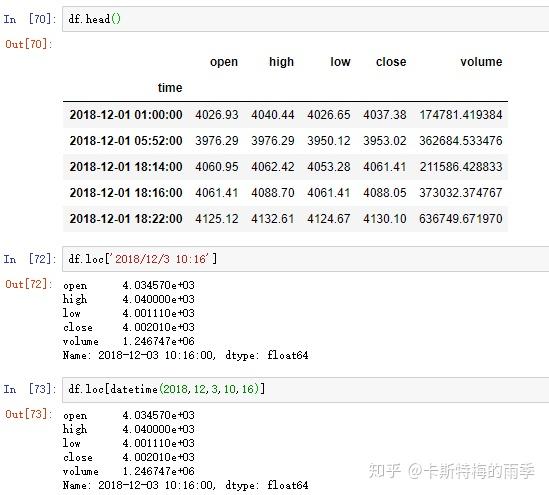

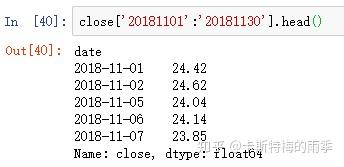

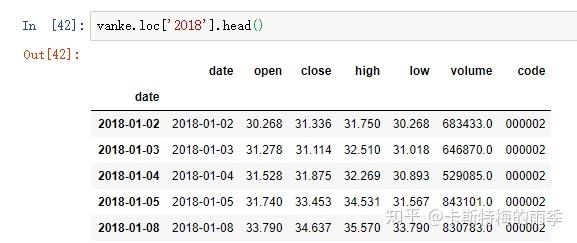

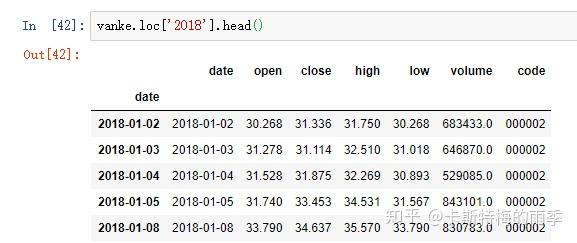

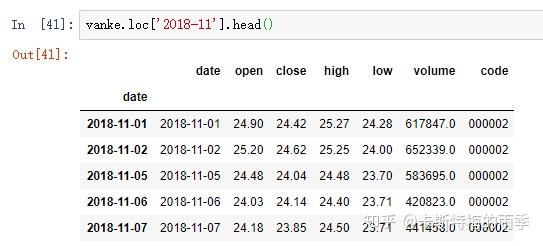

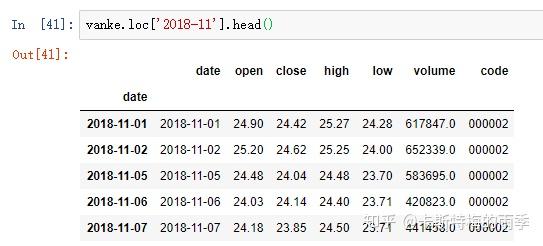

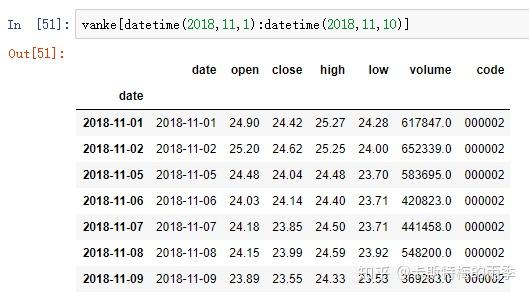

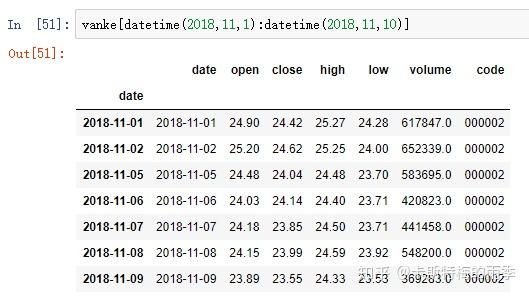

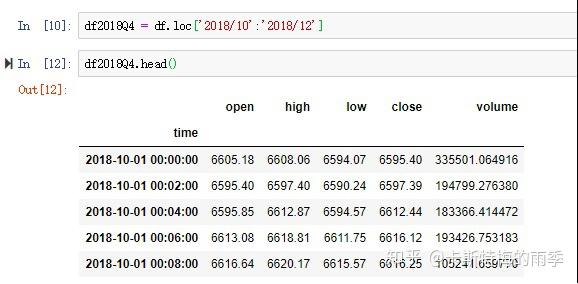

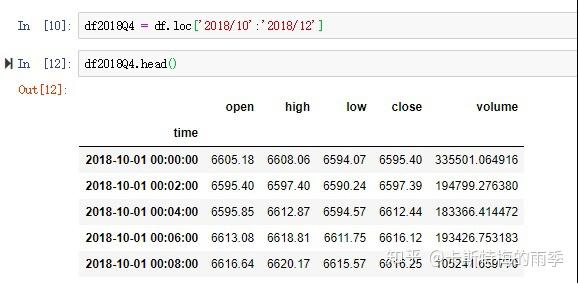

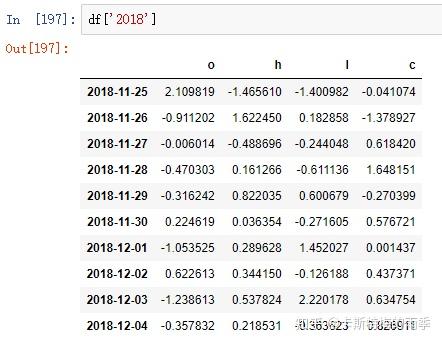

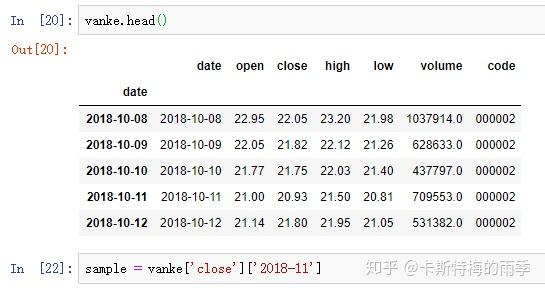

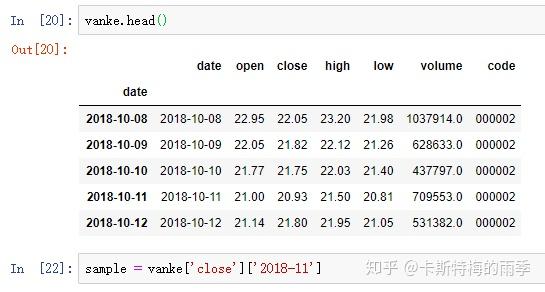

对于较长的时间序列,只需要传入“年”或“年月”即可轻松选取数据的切片:

(相当于 close['20181101':'20181130'])

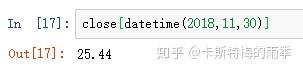

或传入datetime

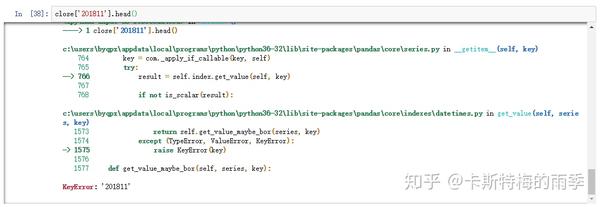

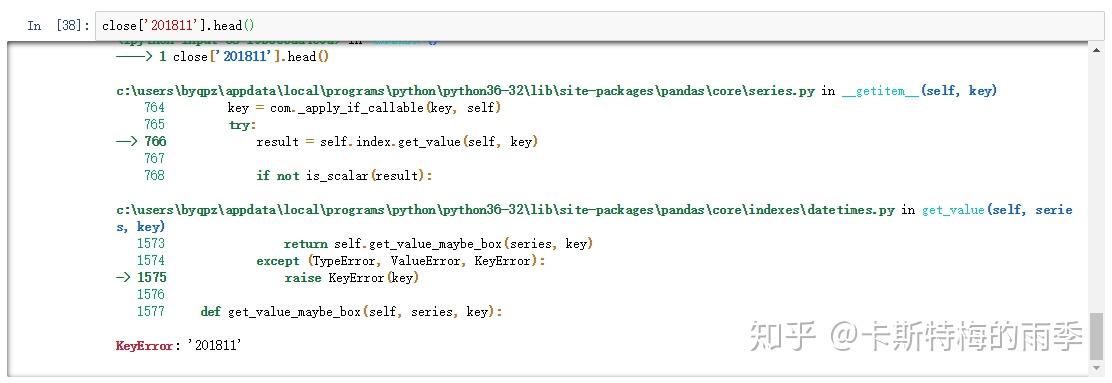

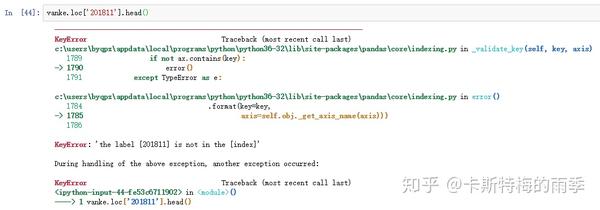

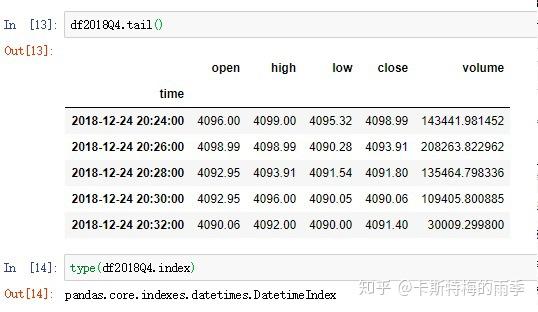

但不能用'201811'这样的形式选取月

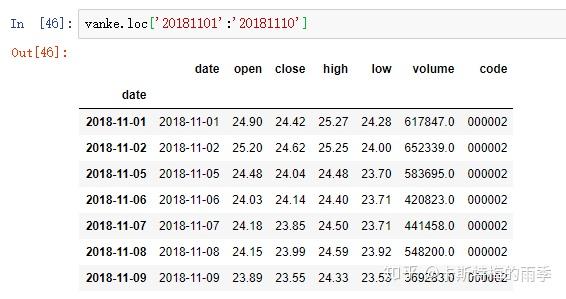

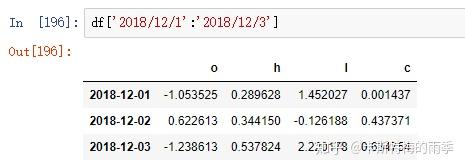

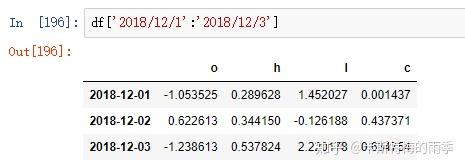

ii)切片

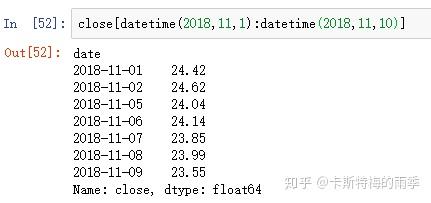

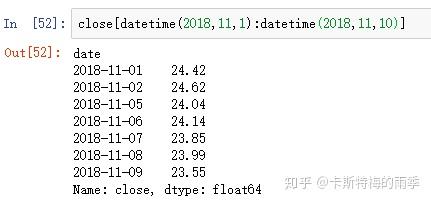

传入字符串日期

传入datetime

索引为DatetimeIndex的DataFrame的索引和切片

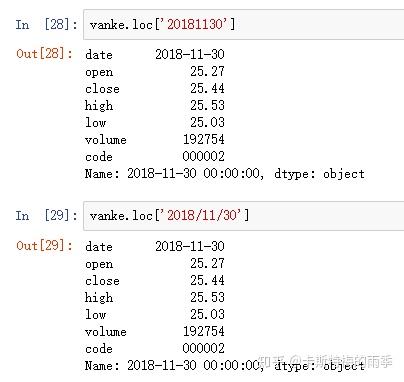

i)索引

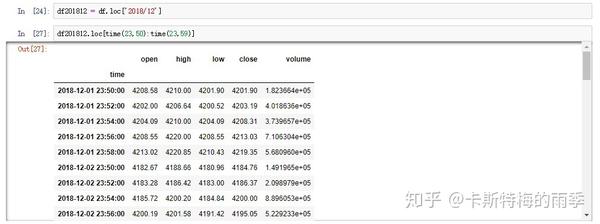

选取年月:

ii)切片

特别一点的切片

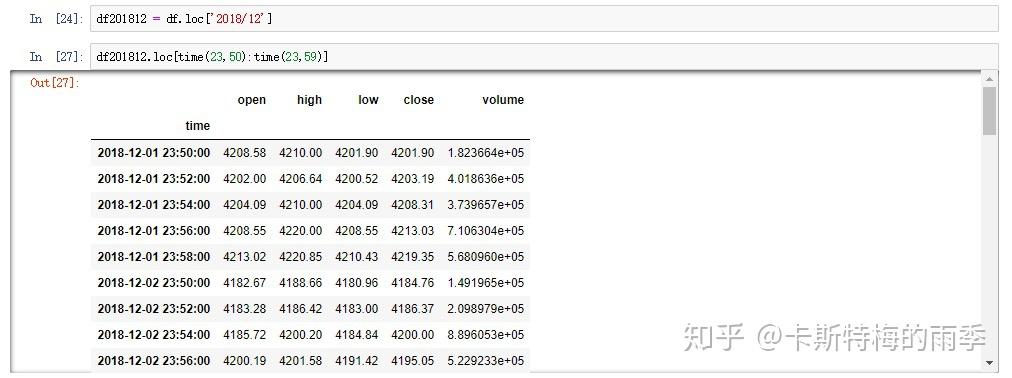

那如果我们想获得每天特定时间段的数据该怎么做呢?

且看下面两个例子

传入time,索引单个时间点,相当于下面的at_time方法

时间段切片,相当于下面的between_time方法

完整的代码如下

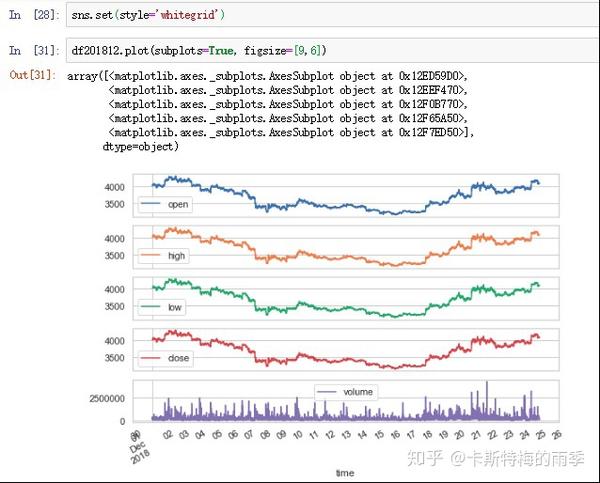

另一个例子更贴近实际应用,假如我们发现某交易对在12月份每天接近24:00时交易量和价格都会出现大幅波动。那么我们现在的目标就是选取每天23:50-23:59的k线数据,然后可视化观察一下是否真的存在这个现象

pandas时间序列的索引和切片是一大利器

IV. 生成PeriodIndex

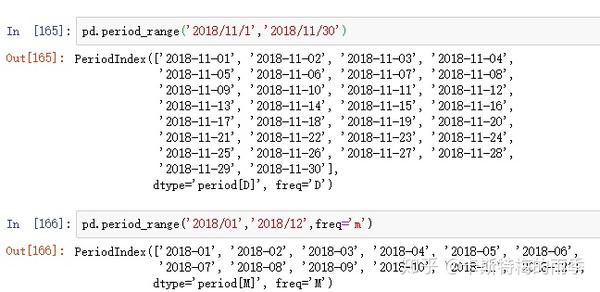

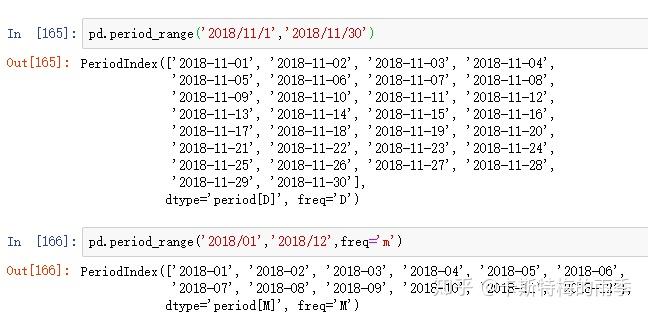

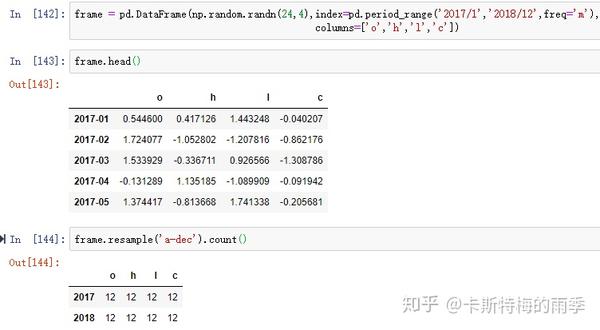

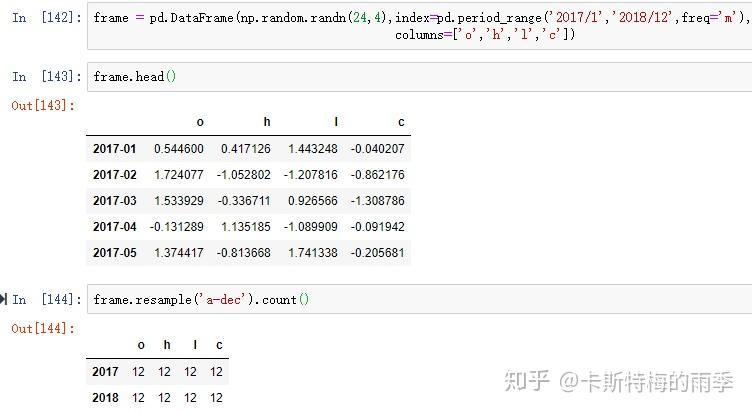

i)pd.period_range

Return a fixed frequency PeriodIndex, with day (calendar) as the default

frequency

period_range(start=None, end=None, periods=None, freq='D', name=None)

start : string or period-like, default None

Left bound for generating periods

end : string or period-like, default None

Right bound for generating periods

periods : integer, default None

Number of periods to generate

freq : string or DateOffset, default 'D' (calendar daily)

Frequency alias

name : string, default None

Name of the resulting PeriodIndex

重点参数:

start

periods

freq

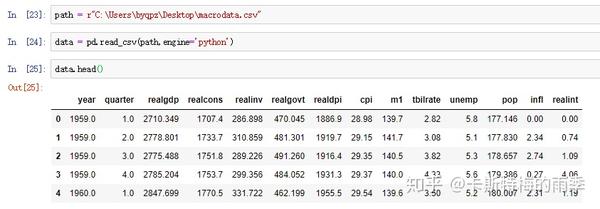

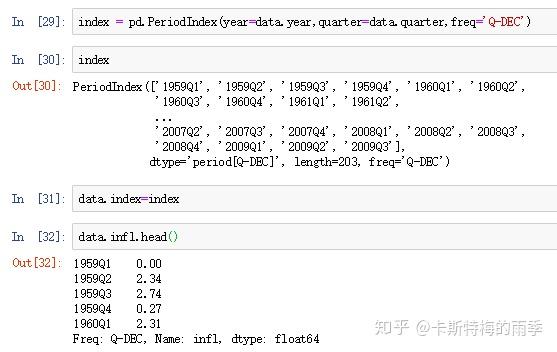

ii)把分开放在不同列中的时间信息合并成一个PeriodIndex

数据:

链接: https:// pan.baidu.com/s/1Pe7Emx t0KPHnsG6SakdF9A

提取码:4dwg

把时间信息分开存放在多列中的数据集适用这种方法

iii)通过pd.PeriodIndex创建

V. 索引为 PeriodIndex 的pandas对象的索引和切片

索引为PeriodIndex的Series的索引和切片

i)索引

ii)切片

索引为PeriodIndex的DataFrame的索引和切片

i)索引

ii)切片

VI. 时期的频率转换

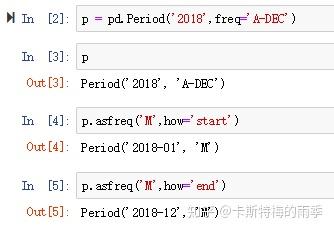

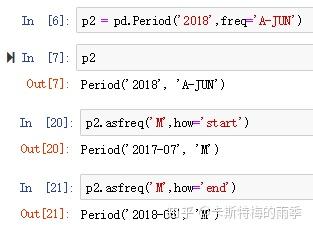

Period和PeriodIndex对象都可以通过asfreq方法转换成其他频率。

i)Period对象转换成别的频率————asfreq

把低频率转化为高频率需要指定how

有些年度并不以12月作为一年的结束,比如财年,此时指定how='start'/'end'得到的月份要根据财年的结束月份来看

而将高频率转换为低频率时,目标时期(pandas中称superperiod)由初始时期(pandasv中称subperiod)所在的位置决定。

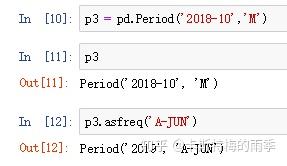

ii)PeriodIndex对象转换成别的频率————asfreq

PeriodIndex的频率转换方式也类似

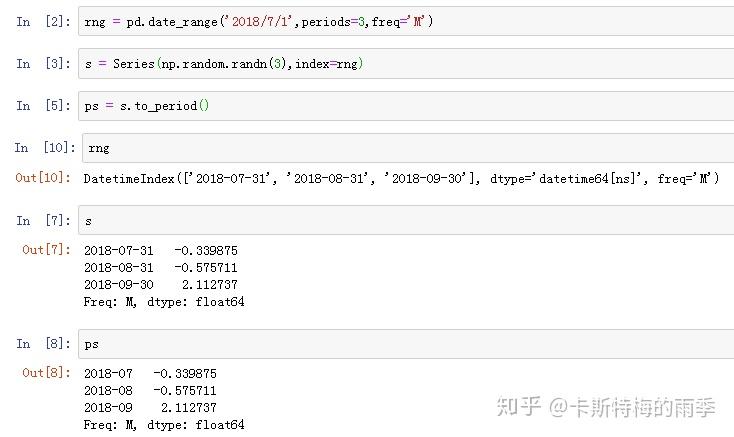

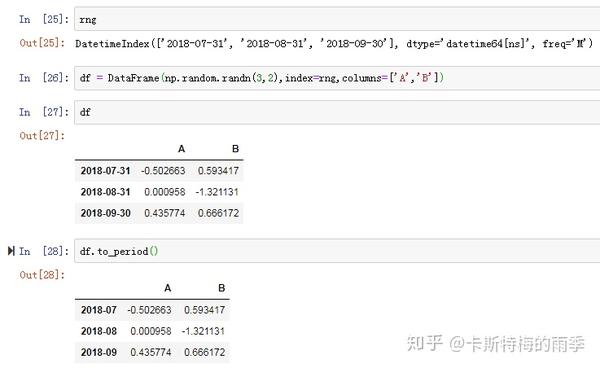

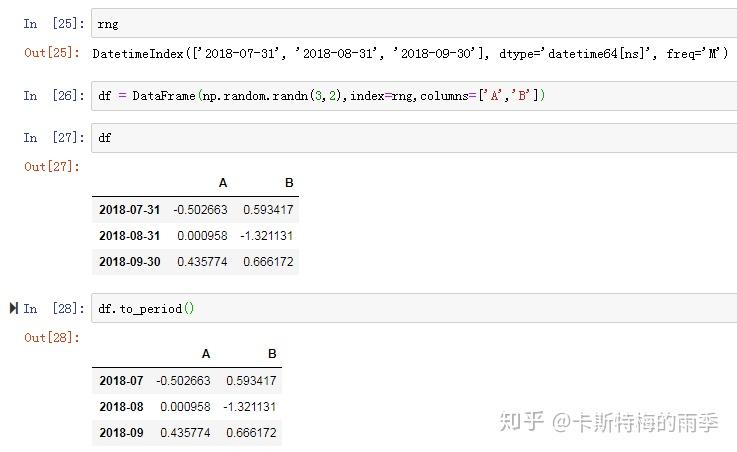

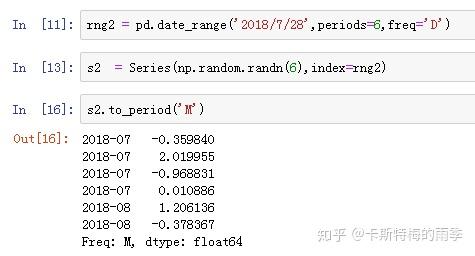

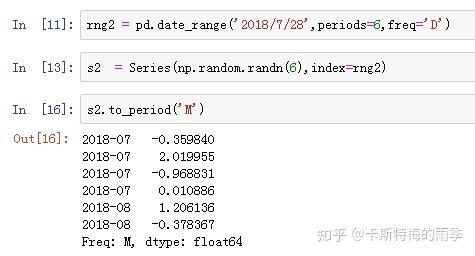

VII. 将DatetimeIndex转换为PeriodIndex及其反向过程

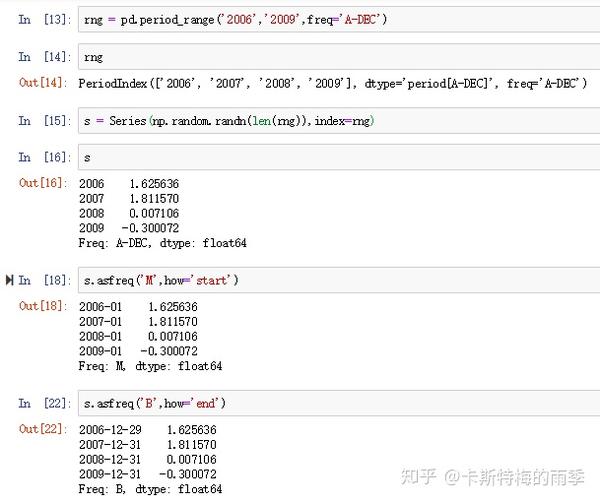

i)将DatetimeIndex转换为PeriodIndex————to_period

通过使用to_period方法,可以将由时间戳索引的Series和DataFrame对象转换为时期索引:

PeriodIndex的频率默认是从DatetimeIndex的频率推断而来的,也可以指定其他频率。

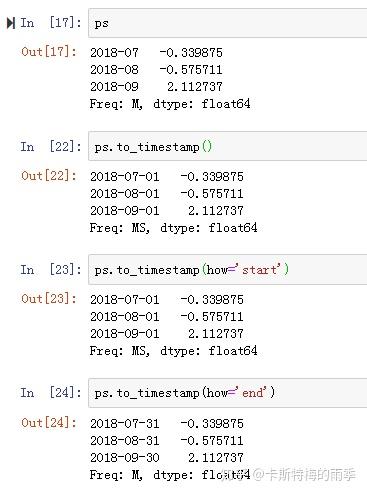

ii)将PeriodIndex转换为DatetimeIndex————to_timestamp

VIII. 重采样(resampling)

(下面这段重采样的定义文字来自 Wes McKinney 《利用Python进行数据分析》)

重采样(resampling)指的是将时间序列从一个频率转换到另一个频率的处理过程。将高频率数据聚合到低频率称为降采样(downsampling),而将低频率数据转换到高频率则称为升采样(upsampling)。 并不是所有的重采样都能被划分到这两个大类中。例如,将W-WED(每周三)转换到W-FRI(每周五)既不是降采样也不是升采样。

Convenience method for frequency conversion and resampling of time

series. Object must have a datetime-like index (DatetimeIndex,

PeriodIndex, or TimedeltaIndex), or pass datetime-like values

to the on or level keyword.

resample(rule, how=None, axis=0, fill_method=None, closed=None, label=None,

convention='start', kind=None, loffset=None, limit=None, base=0,

on=None, level=None)

rule : string

the offset string or object representing target conversion

axis : int, optional, default 0

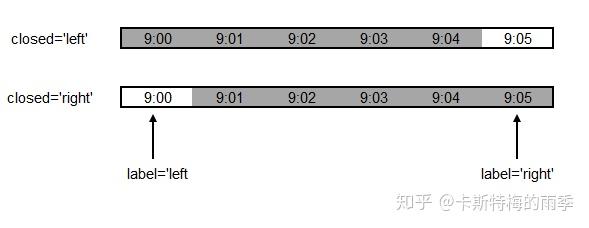

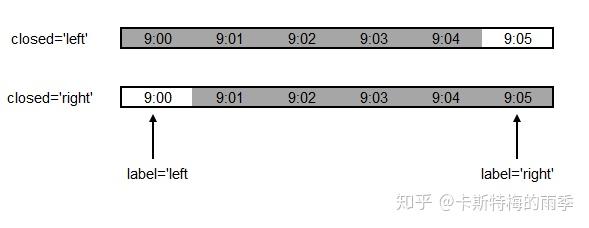

closed : {'right', 'left'}

Which side of bin interval is closed. The default is 'left'

for all frequency offsets except for 'M', 'A', 'Q', 'BM',

'BA', 'BQ', and 'W' which all have a default of 'right'.

label : {'right', 'left'}

Which bin edge label to label bucket with. The default is 'left'

for all frequency offsets except for 'M', 'A', 'Q', 'BM',

'BA', 'BQ', and 'W' which all have a default of 'right'.

convention : {'start', 'end', 's', 'e'}

For PeriodIndex only, controls whether to use the start or end of

当重采样时期时,将低频率转换到高频率所采用的约定('start'或'end'),

默认为'start'

kind: {'timestamp', 'period'}, optional

Pass 'timestamp' to convert the resulting index to a

``DateTimeIndex`` or 'period' to convert it to a ``PeriodIndex``.

By default the input representation is retained.

聚合到时期('Period')或时间戳('timestamp'),默认聚合到时间序列的索引类型

loffset : timedelta

Adjust the resampled time labels

面元标签的时间校正值,比如'-1s'/Second(-1)用于将聚合标签调早1秒

base : int, default 0

For frequencies that evenly subdivide 1 day, the "origin" of the

aggregated intervals. For example, for '5min' frequency, base could

range from 0 through 4. Defaults to 0

on : string, optional

For a DataFrame, column to use instead of index for resampling.

Column must be datetime-like.

level : string or int, optional

For a MultiIndex, level (name or number) to use for

resampling. Level must be datetime-like.

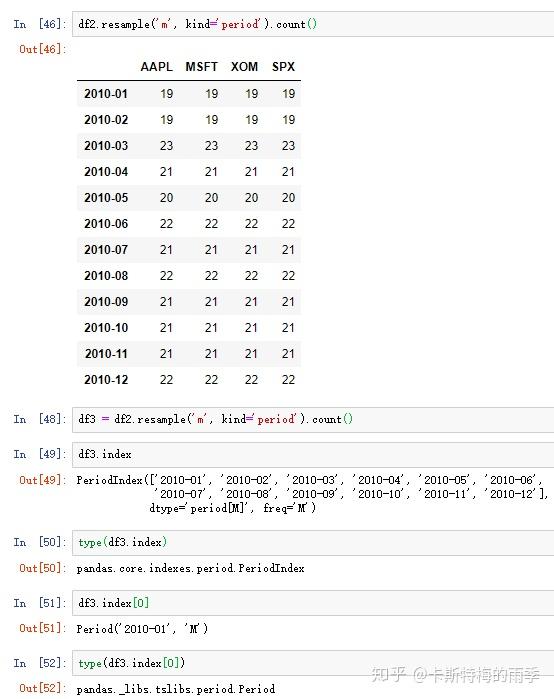

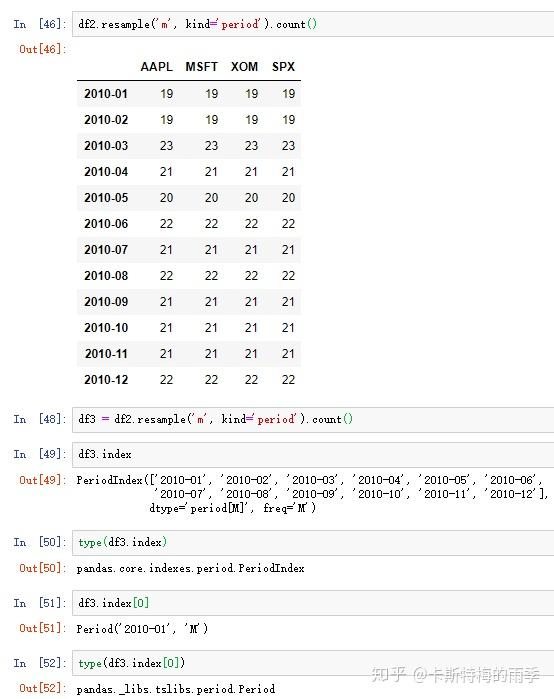

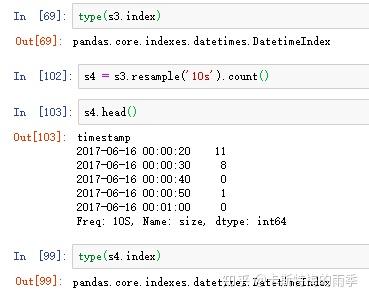

DatetimeIndex Resamping

i)降采样

(下面这段定义文字摘录自 Wes McKinney 《利用Python进行数据分析》)

将数据聚合到规整的低频率是一件非常普通的时间序列处理任务。待聚合的数据不必拥有固定的频率,期望的频率会自动定义聚合的面元边界,这些面元用于将时间序列拆分为多个片段。 各时间段都是半开放的。一个数据点只能属于一个时间段,所有时间段的并集必须能组成整个时间帧

example 1:

example 2:

"1分钟"数据被转换为"5分钟"数据的处理过程:

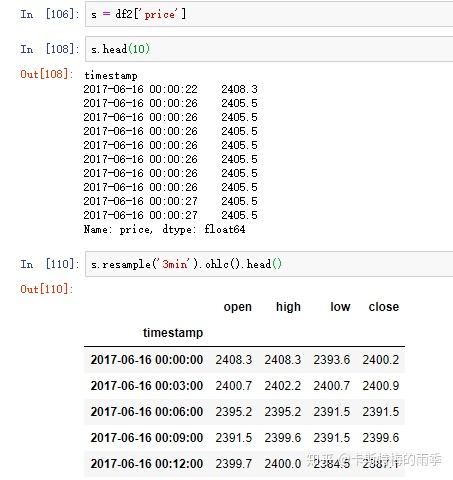

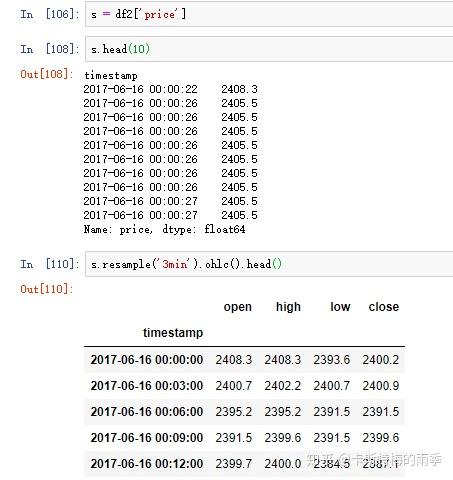

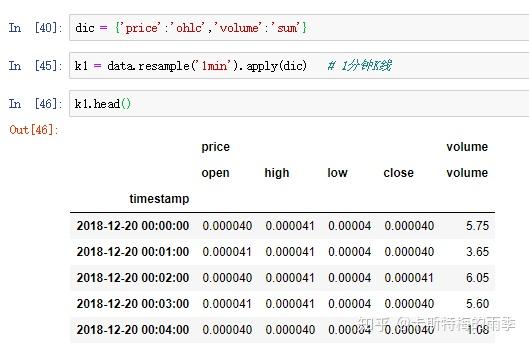

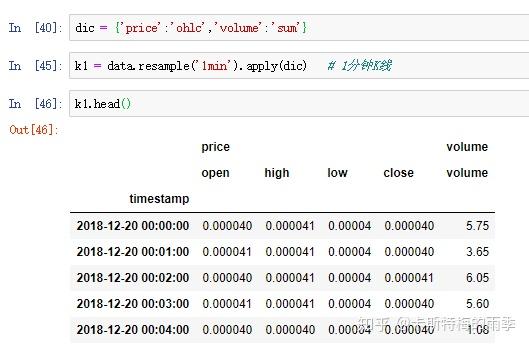

除了可以对resampler对象调用mean、count、sum、min、max、median、first、last等函数外,还可以对其调用ohlc,即计算各面元的四个值:open(开盘价)、high(最高价)、low(最低价)、close(收盘价)。对resampler对象调用 .ohlc() 即可得到含有这四种聚合值的DataFrame

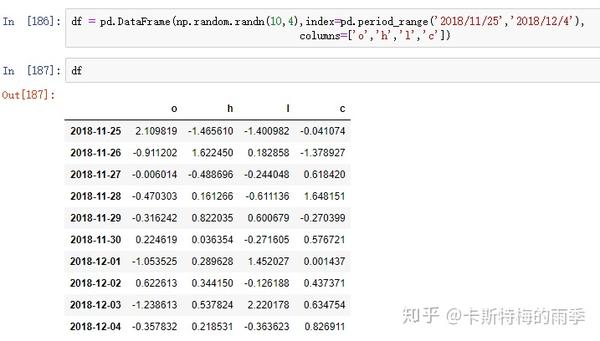

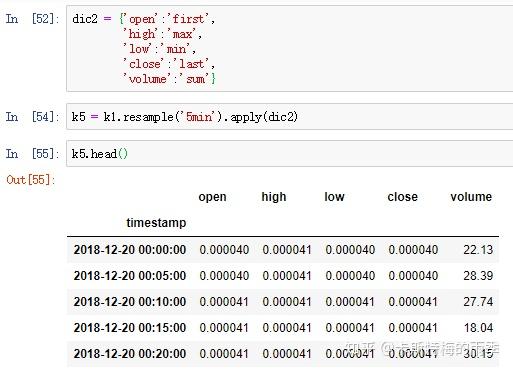

更自由的函数定义方式是我们之前提到过的 apply方法, 对其传入"列名:函数名"键值对的字典,我们就可以对不同的列定义不同的聚合函数。下面结合K线图的生成及转化简单介绍一下:

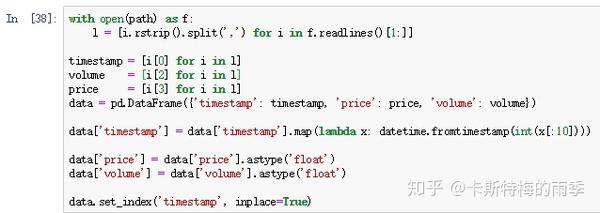

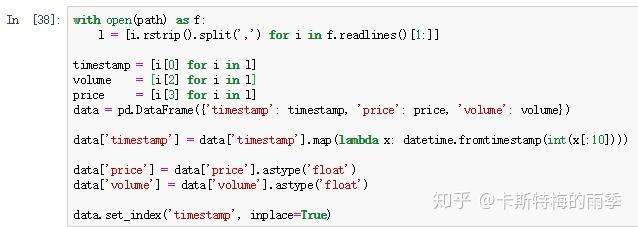

原始数据like this,字段分别为时间,交易类型,量,价格

先简单处理一下

处理后的数据如下所示

接下来降采样,用apply(dict)的方式生成一分钟K线,注意看

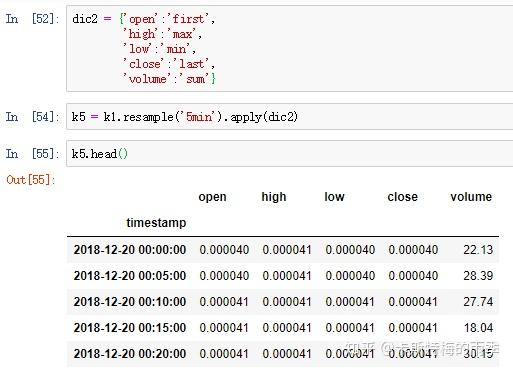

然后是K线转化,但因为我们前面得到是一个MultiIndex的df,所以需要先处理一下columns

接下来是类似的操作

除了resample()方法,还可以使用groupby()方法对数据进行降采样。如果需要根据月份进行分组,只需传入一个能够访问时间序列的索引上的这些字段的函数即可:

因为重采样中降采样出现的频率会更高,所以这里介绍得更详细一些。

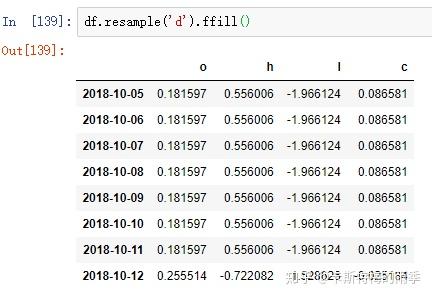

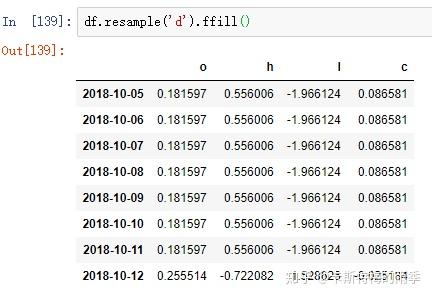

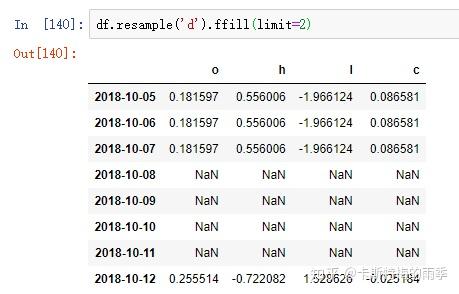

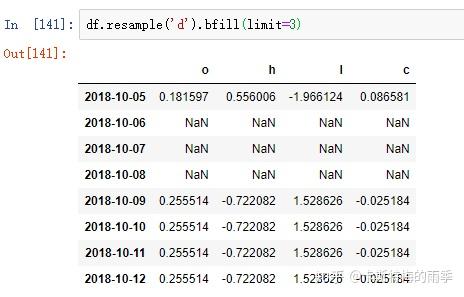

ii)升采样和插值

如果是将数据从低频转换到高频,就无需聚合。

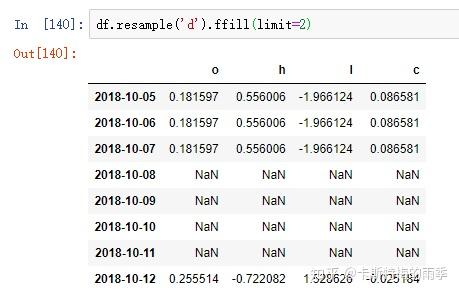

升采样默认会引入缺失值,如果想用前后数据填充缺失,调用ffill,bfill等方法即可(resampling的填充和插值方式跟fillna和reindex的一样),也可以在其中传入limit参数,限制填充的距离

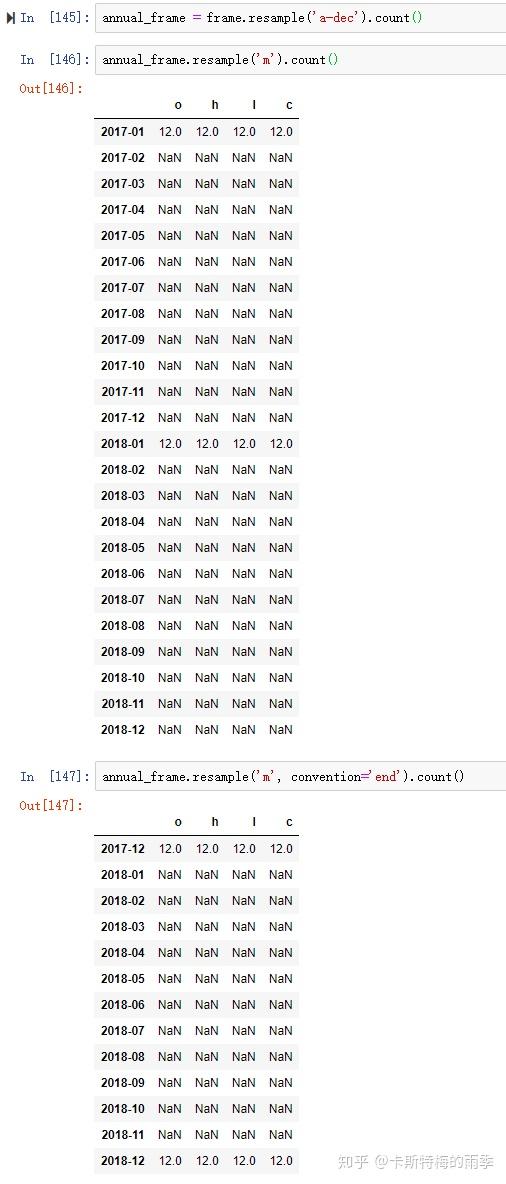

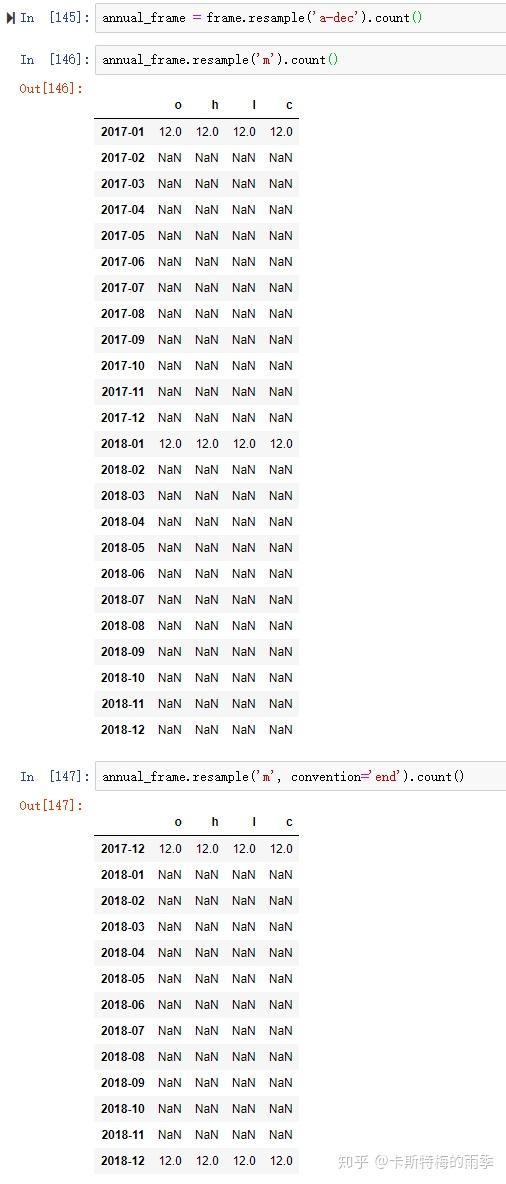

PeriodIndex Resamping

i)降采样

对索引是PeriodIndex的数据进行降采样

ii)升采样和插值

convention默认为'start',也可以手动设置为'end'

IX. 移动窗口函数(moving window function)

Provides rolling window calculations.

rolling(window, min_periods=None, center=False, win_type=None, on=None, axis=0, closed=None)

window : int, or offset

Size of the moving window. This is the number of observations used for

calculating the statistic. Each window will be a fixed size.

If its an offset then this will be the time period of each window. Each

window will be a variable sized based on the observations included in

the time-period. This is only valid for datetimelike indexes. This is

new in 0.19.0

min_periods : int, default None

Minimum number of observations in window required to have a value

(otherwise result is NA). For a window that is specified by an offset,

this will default to 1.

center : boolean, default False

Set the labels at the center of the window.

win_type : string, default None

Provide a window type. If ``None``, all points are evenly weighted.

See the notes below for further information.

on : string, optional

For a DataFrame, column on which to calculate

the rolling window, rather than the index

closed : string, default None

Make the interval closed on the 'right', 'left', 'both' or

'neither' endpoints.

For offset-based windows, it defaults to 'right'.

For fixed windows, defaults to 'both'. Remaining cases not implemented

for fixed windows.

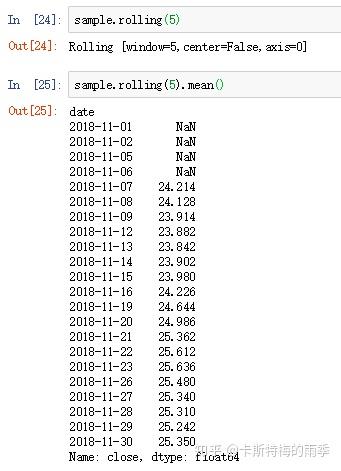

i)window为整数

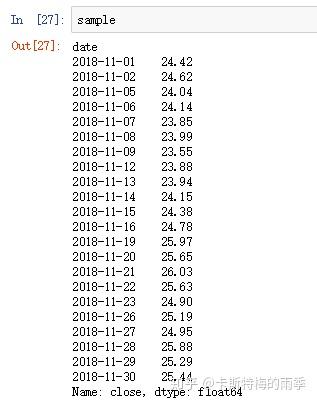

如果只传入一个表示移动窗口大小的整数(这里是5),sample.rolling(5).mean()计算的就是11月连续5天收盘价的算数平均值,此时min_periods默认是None

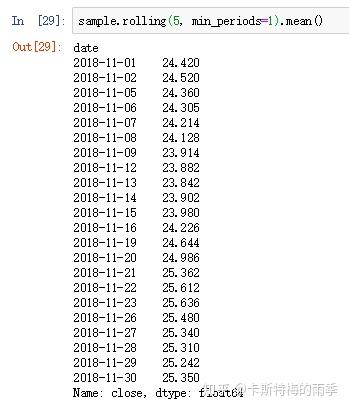

当然,我们可以手动设置min_periods,如果min_periods=1,前面11-1、11-2、11-5、11-6对应的值就不会为空了,它们分别会变成24.42、(24.42 + 24.62)/2、(24.42 + 24.62 + 24.04)/3、(24.42 + 24.62 + 24.04 + 24.14)/4。换言之,在window是一个整数的情况下,如果观测值的数量不足移动窗口的大小,且设置了min_periods,则从长度满足min_periods的位置开始计算统计量。

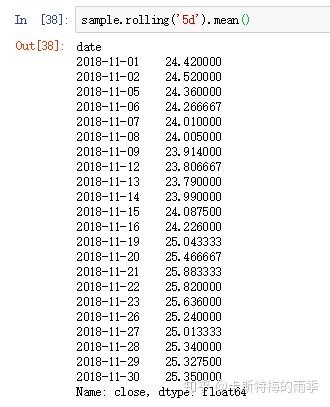

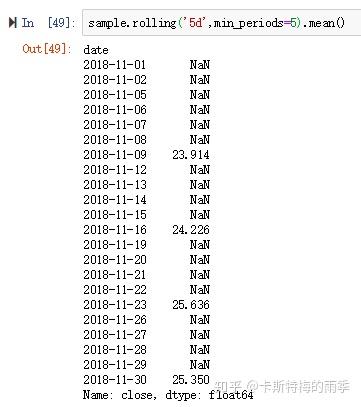

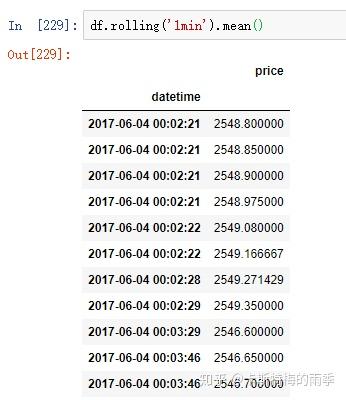

ii)window为日期偏移量

而如果向window传入的是日期偏移量,且索引为DatetimeIndex,那么每个移动窗口的大小就是对应的偏移量的大小。当window是一个日期偏移量的时候,min_periods默认为1。此时11-5、11-6、11-7对应的分别就是(24.42+24.62+24.04)/3、(24.62+24.04+24.14)/3、(24.04+24.14+23.85)/3,因为对应的是日历日嘛。那能不能传入工作日呢?不行,因为BusinessDays并不是一个固定的频率

特别需要注意的是,当window为偏移量的时候,closed默认为右侧关闭。例如下面这个demo, 00:03:29 对应移动窗口是 00:02:30 至 00:03:29 ,,所以不计算 00:02:29 的价格在内

如果对DataFrame调用rolling().mean()之类的函数时,会将转换应用到所有的列上:

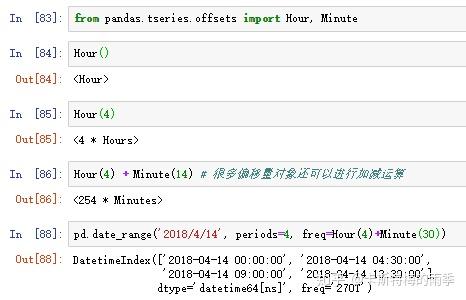

X. 频率和时间、日期的偏移

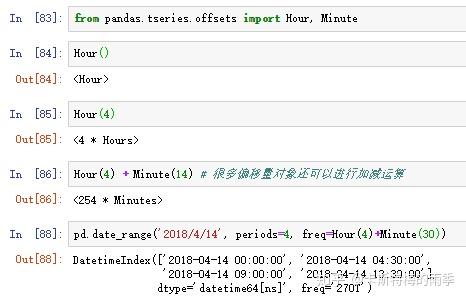

i)显式创建pd.tseries.offsets对象

下面这段pandas基本频率的描述来自Wes McKinney 《利用Python进行数据分析》

pandas中的频率是由一个基础频率(base frequency)和一个乘数组成的。基础频率都用一个字符串别名表示,比如'M'表示每月,'H'表示每小时。对于每个基础频率,都有一个被称为日期偏移量(date offset)的对象与之对应。

ii)使用字符串别名

其实我们可以用'4h30min'这样的字符串别名替代Hour(4)+Minute(30)

换个偏移量

iii)时间、日期的偏移

>>>df = pd.read_csv(path, engine='python', encoding='utf_8_sig',index_col='time',parse_dates=True)

>>>s = '2018-12-08 00:08'

>>>d = parse(s) + Minute(2)

Timestamp('2018-12-08 00:10:00')

>>>df.loc[d]

open 3.341530e+03

high 3.343600e+03

low 3.335010e+03

close 3.339980e+03

volume 2.214765e+05

OBV 1.255913e+06